Shareholders

Vicat Shareholders and Investors Service:

Tél : +33 1 58 86 86 86

Email : relations.investisseurs@vicat.fr

Shareholder information

Web site : www.vicat.fr

Symbol : VCT

ISIN Code: FR0000031775

Euroclear France : 816

Bloomberg : VCT.PA

Reuters : VCTP.PA

To become a shareholder of the Vicat Group, please consult your financial adviser or broker.

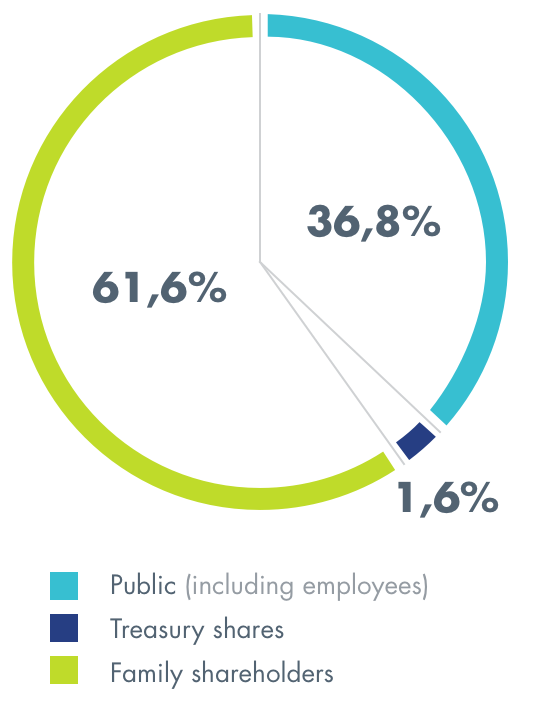

Capital structure

Share capital

As of December 31, 2021, the company’s share capital amounted to 179,600,000 euros, consisting of 44,900,000 shares with par value of four euros each.

The Company's shares are traded on the Eurolist market of Paris' Euronext Stock Exchange, Compartment A.

Its shares have also been eligible for the Deferred Settlement Service since February 2008.

Dividend

Based on results in 2021, and confident in the Group’s ability to sustain its ongoing development, the Board of Directors has decided to propose that the Annual General Meeting of shareholders on April 13, 2022. Dividend increase of 1.65 euros per share.

Share details

Place listed

Euronext Paris

Exchange segment

Compartiment A

Share code

FR00000 31775 –VCT

Sector classification

Matériaux et accessoires de construction

Registered shares

Tour Manhattan 6 place de l’Iris 92095 La Défense Cedex

Tickers

Reuters VCT PA et Bloomberg VCT FP